Table Of Content

Additionally, interest rates offered for VA loans often turn out to be lower than those offered for conventional loans. If you get a $200,000 mortgage with a 15 year fixed rate at 5%, your monthly payments will be $1,582 (excluding taxes and insurance). The 29/41 rule is important to know when thinking about your mortgage qualification because DTI helps lenders determine your ability to pay your mortgage. Although higher housing expenses and DTIs are allowed under many loan types (including conventional, FHA, USDA and VA loans), the 29/41 rule provides a good starting point.

How does credit score impact affordability?

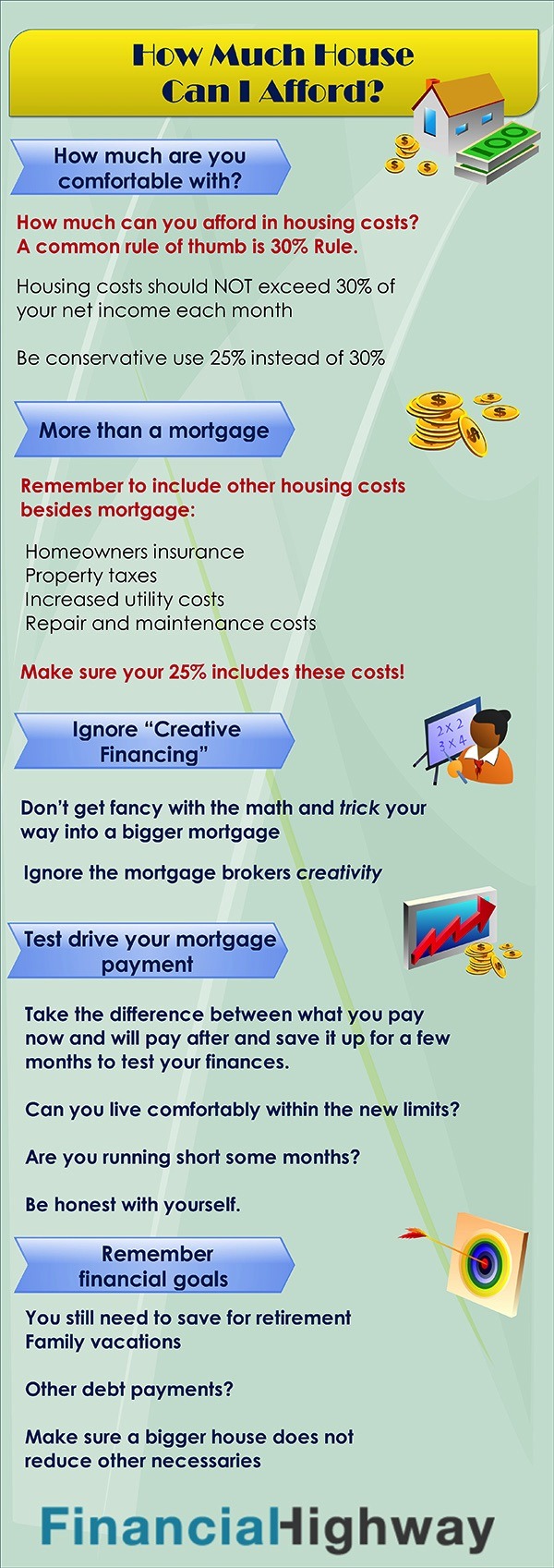

For most home buyers, this means choosing a home and mortgage loan that will keep your total monthly mortgage payment at 29% or less of your gross monthly income. Make sure your mortgage payment (principal, interest, property taxes and homeowners insurance) is no more than 29% of your gross monthly income. Also make sure your total monthly debt (mortgage plus car loans, student debts, etc.) is no more than 41% of your gross monthly income.

How to use our mortgage affordability calculator

Depending upon your property location, property type, and loan amount, you may have other monthly or annual expenses such as mortgage insurance, flood insurance, or homeowner association fees. LendingTree’s calculator defaults to a 30-year fixed-rate mortgage, but there’s a 15-year fixed-rate term option if you want to save on interest charges and can afford a higher monthly payment. These are all solid choices, except for making only the minimum payments on your bills. Having less debt can improve your credit score and increase your monthly cash flow. They will also decrease how much interest you pay on those debts. A jumbo loan is used when the mortgage exceeds the limit for Fannie Mae and Freddie Mac, the government-sponsored enterprises that buy loans from banks.

Income

How Much House Can I Afford On A $200K Salary? - Bankrate.com

How Much House Can I Afford On A $200K Salary?.

Posted: Tue, 11 Jul 2023 07:00:00 GMT [source]

Also, if you already calculated all expenses on a house and get a certain number, say, $1,450, you should try and cut down your $600 monthly payments by $250 for a better chance at a loan. Once you’ve plugged in all your info, you’ll get an estimated number for the maximum amount you can pay for a house, plus your estimated monthly mortgage payment. This makes FHA loans ideal for those who might have less income or a shorter credit history. Get pre-qualified by a lender to see an even more accurate estimate of your monthly mortgage payment.

How much is homeowners insurance and what does it cover?

Both the upfront fee and the annual fee will detract from how much home you can afford. You’ll often hear that you should have three to six months’ worth of living expenses saved to cover emergencies. As a homeowner, you’d be wise to have six months to two years’ worth of living expenses saved. You never know when a global pandemic might wreak havoc on your ability to earn a living and pay for your home.

The mortgage interest rate is the amount charged by a lender in exchange for loaning money to a buyer. It is expressed as a yearly percentage of the total loan amount but is calculated into the monthly mortgage payment. If you don’t qualify for a VA loan or a 0% down payment mortgage program, most buyers will have to give a down payment on their potential home.

How Much Should I Have Saved When Buying a Home?

What if you have a student loan in deferment or forbearance and you’re not making payments right now? Many homebuyers are surprised to learn that lenders factor your future student loan payment into your monthly debt payments. After all, deferment and forbearance only grant borrowers a short-term reprieve—much shorter than your mortgage term will be. Use the affordability calculator to see how your down payment affects your home affordability estimate and your monthly mortgage payment. Once you close on your home loan, your monthly mortgage payment may well be the biggest debt payment you make each month, so it’s important to make sure you can afford it. Your monthly payment and down payment are probably the two biggest factors in determining how much you can afford.

Create your list of monthly expenses

Buyers Need A Six-Figure Salary To Comfortably Afford A Home, Zillow Finds - Forbes

Buyers Need A Six-Figure Salary To Comfortably Afford A Home, Zillow Finds.

Posted: Wed, 27 Mar 2024 07:00:00 GMT [source]

And from applying for a loan to managing your mortgage, Chase MyHome has everything you need. If you obtain home financing, you’ll repay more than the amount you borrowed because the amount you repay is determined by several factors, including the interest and loan amount. Understanding the difference — and then using a home affordability calculator to crunch some numbers — will help you decide how much house you can really afford.

Chase Home Lending

But real estate experts warn against waiting for interest rates to decline before purchasing a house, as home prices on-average will continue to increase in value. With a 20% down payment, only six metro areas are affordable for the median earner, the data revealed. Make a mortgage payment, get info on your escrow, submit an insurance claim, request a payoff quote or sign in to your account. Go to Chase home equity services to manage your home equity account. We'll send you disclosures listing your loan terms as well as estimated payments, and your application will be reviewed by an underwriter.

When you sign your mortgage loan, the interest rate you agree to pay influences the cost of your monthly payments, the size of your down payment and the overall cost of your loan. Affordability can also be influenced by whether you choose a fixed-rate or adjustable-rate mortgage. When you’re shopping around for a house — and trying to decide how much you can afford to spend — having a solid grasp of your mortgage interest rate is vitally important. Find out how much you can afford with our mortgage affordability calculator.

You need to calculate how much house you can afford while considering a wide range of loan options. Your reserve could cover your mortgage payments - plus insurance and property tax - if you or your partner are laid off from a job. It gives you wiggle room in case of an emergency, which is always helpful. Homeownership comes with unexpected events and costs (roof repair, basement flooding, you name it!), so keeping some cash on hand will help keep you out of trouble. Key factors in calculating affordability are 1) your monthly income; 2) cash reserves to cover your down payment and closing costs; 3) your monthly expenses; 4) your credit profile. The amount you'll need to close your loan includes your down payment, closing costs, and prepaid escrow amounts for property taxes and insurance.

According to the data, a median home in California sells for $798,854. After a 20% down payment, the monthly mortgage payment costs about $5,183, or $62,197 annually. As a homeowner, you’ll pay property tax either twice a year or as part of your monthly home payment. This tax is a percentage of a home’s assessed value and varies by area. For example, a $500,000 home in San Francisco, taxed at a rate of 1.159%, translates to a payment of $5,795 annually.It’s important to consider taxes when deciding how much house you can afford. When you buy a home, you will typically have to pay some property tax back to the seller, as part of closing costs.

They are basic debt-to-income ratios (DTI), albeit slightly different and explained below. For more information about or to do calculations involving debt-to-income ratios, please visit the Debt-to-Income (DTI) Ratio Calculator. This is a separate calculator used to estimate house affordability based on monthly allocations of a fixed amount for housing costs. There are two House Affordability Calculators that can be used to estimate an affordable purchase amount for a house based on either household income-to-debt estimates or fixed monthly budgets. Explore mortgage options to fit your purchasing scenario and save money. This depends on how much you intend to put up as a down payment.

However, there are many ways to qualify whether you’re a veteran, active duty service member, reservist or member of the National Guard. You can get a free credit report once per year from each of the three major credit bureaus. You may also access your credit report for free under certain conditions, for example, if you’re the victim of identity theft. Input these numbers into our Home Affordability Calculator to get a clear idea of your homebuying budget. Our partners cannot pay us to guarantee favorable reviews of their products or services.

We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Conventional loans can come with down payments as low as 3%, although qualifying is a bit tougher than with FHA loans. "People in New York or D.C. are paid higher salaries than people in states with a lower cost of living, such as Arkansas or Louisiana." "COVID relief policies bolstered the economy, leading to boosted stock prices, real estate and savings," Murray told CBS MoneyWatch. "These conditions were especially favorable for the wealthiest of Americans, who experienced dramatic income increases, especially considering the fact that many companies saw record profits." In summary, Los Angeles, CA, is a city with a rich history, diverse geography, and a dynamic economy.

Want a quick way to determine how much house you can afford on a $40,000 household income? Use our mortgage income calculator to examine different scenarios. That’s a big deal, because mortgages backed by the Department of Veterans Affairs typically don’t require a down payment. The NerdWallet Home Affordability Calculator takes that major advantage into account when computing your personalized affordability factors. To calculate how much house you can afford, we’ve made the assumption that with at least a 20% down payment, you might be best served with a conventional loan.

No comments:

Post a Comment